now loading...

The Asian investment grade market faces some near-term challenges, such as the impact of US trade actions. However, the market appears resilient, with very few issuers directly affected by the US tariffs. At the same time, China, which accounts for half of the market, continues with its deleveraging campaign toward more sustainable credit metrics.

Going forward, we believe Asian investment grade credit will continue to be a core fixed income market anchored by these three main reasons.

Strong fundamentals

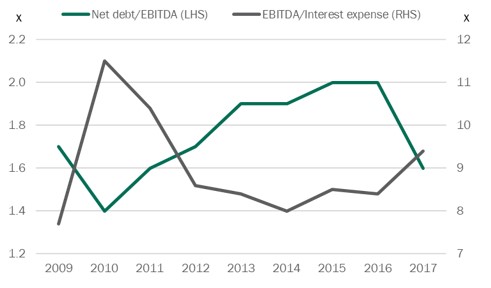

The fundamentals of the Asian investment grade credit market remain solid and have been improving since 2015. For instance, net debt to EBITDA continued its decline to about 1.7 times ( x ) in 2018 from over 2x in 2015. EBITDA and other profitability margins have reached new highs since the 2008 financial crisis. And interest coverage is strong at 8x to 9x.

On the back of the deleveraging campaign in China, there has been a notable improvement in the state-owned sector, where discipline in cost cutting, mergers and acquisitions, and capital expenditures is helping improve credit metrics. This is also the case for Korean, Hong Kong, and other issuers. Credit rating movements also reflect an overall improvement in Asian investment grade fundamentals, with the rating upgrade/downgrade ratio standing at 4.2x in 2018 from 0.52x in 2017.1

Credit Metrics Are Improving

Source: J.P. Morgan and PineBridge, as of 4 June 2018. For illustrative purposes only. We are not soliciting or recommending any action based on this material.

Attractive valuation versus developed market ( DM ) investment grade credits

Asian IG currently offers a 35-basis-point ( bp ) pickup over developed market IG for the same average credit rating and is 2.3 years shorter in duration, which makes Asian IG a diversifier to the more rate-sensitive developed market IG market. The shorter duration and better spread cushion of Asia IG has also resulted in lower volatility compared with DM IG credits.

Valuations Are Attractive and Average Durations Are Shorter

|

Avg. rating |

Avg. duration |

Avg. spread ( bps ) |

Last 3-year annualized return volatility |

|

|

Asia IG credit |

A3 |

4.8 |

141 |

2.0% |

|

Global DM IG Credit |

A3 |

7.1 |

106 |

3.8% |

Source: BoAML ICE, as of 31 August 2018.

Volatility and Sensitivity to Rate Hikes Are Lower

Persistent strong technical factors

Coming from a very low base, volatility can increase going forward, but it is important to note that this will be mitigated by the fact that Asia has a growing money pool. In the past 10 years, we have seen a consistently higher share of the Asian credit market owned by Asian buyers.

Today, Asian buyers are 78% of the market, which helps to anchor the market and shelter it from fickle "tourist" investors. Asian investors tend to have a home bias, purchasing issuers they understand and know. Although Asia is a high issuance market, on a net basis, the Asian credit market remains stable. This is displayed in the better risk-adjusted returns of Asian US dollar-denominated bonds generally, with a Sharpe ratio of 1.67, as opposed to the emerging markets and US IG credit bonds, which have a Sharpe ratio of 1.02.

Additionally, the Asian investment grade segment has a lower duration profile, making it more defensive for investors concerned about interest rate risk. It is also important to mention that global allocation into Asia is expected to increase with time, given the natural growth of Asia's share in the global economy and indexes.

Domestic Buyers Dominate in Asian Credit

Supported by strong and persistent technical factors, as well as resilient fundamentals, the Asian investment grade credit segment continues to outperform a large number of its peers, and we expect it will retain its status as a core fixed income holding. While not without risks, our investment thesis favours greater issuer differentiation as multiyear credit trends emanate from China's economic transformation and Asia's continued economic rise.

Arthur Lau, co-head of EM fixed income, head of Asia ex Japan fixed income, PineBridge Investments, Hong Kong.

Lau is a member of the global bond management team participating in strategy development and execution, monitoring developments in the primary and secondary markets and portfolio monitoring.