now loading...

During the most recent episode of emerging market sell off, different markets in Asia experienced different ebbs and flows. For instance, India, Indonesia, and Malaysia suffered from capital outflows, whereas Thailand and the Philippines performed fairly well in the selloff. One market, however, namely Taiwan, seems to be ring-fenced from all these external shocks.

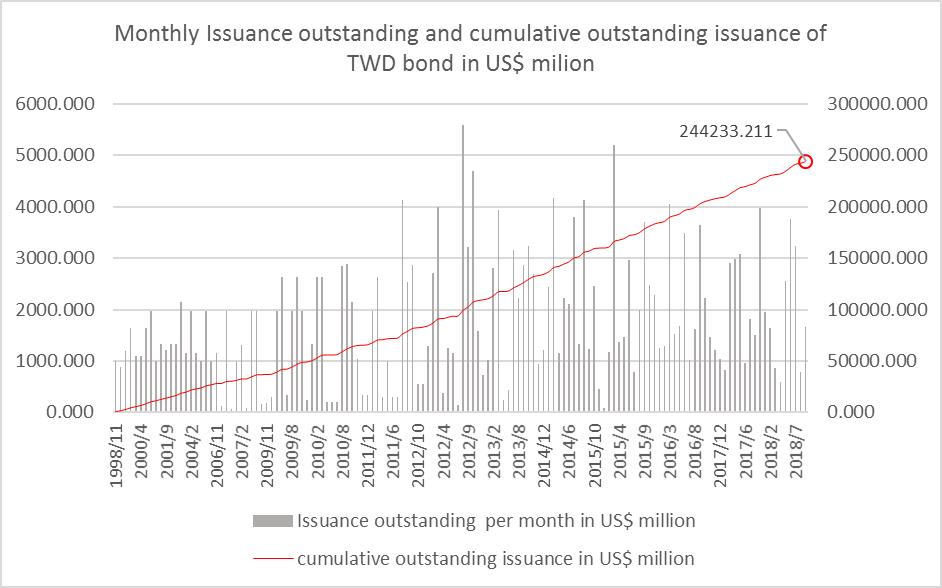

According to data from Taipei Exchange, the size of Taiwan dollar denominated bond market has grown from US$1.877 billion in 1998 to US$244.233 billion in 2018. Within twenty years, the market grew by more than 130 times ( Fig. 1 ).

Fig. 1

Source: Taipei Exchange

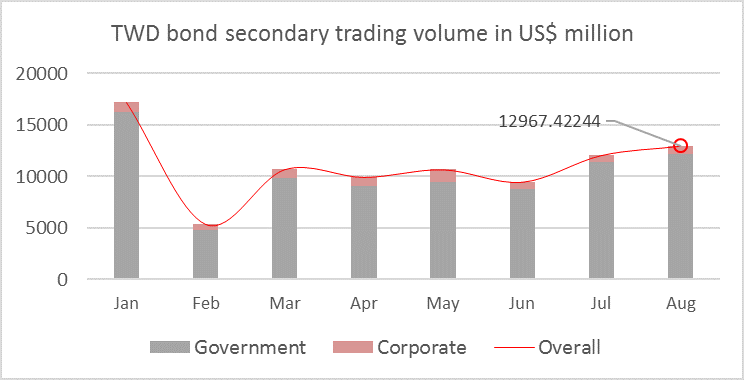

Among the outstanding issuance, three-quarters of the outstanding bonds are government bonds, amounting to US$183 billion according to the latest data available, which is already comparable to Indonesia's total bond market size. When considering the volume of secondary market trading, it becomes apparent that trading activity is pitifully low.

The secondary trading volume in the Taiwan dollar denominated market is only US$12 billion ( fig. 2 ), just 5% of the total market size. In other words, over 90% of the bonds were not traded but remained in the hands of investors. Lack of accurate data prevents the compilation of an investor profile of the Taiwan dollar denominated bond holding, but the behaviour of investors suggests that insurance companies in Taiwan are the dominant buyside participants, as they generally adopt a buy-and-hold strategy in the bond market.

Fig. 2

Source: Taipei Exchange

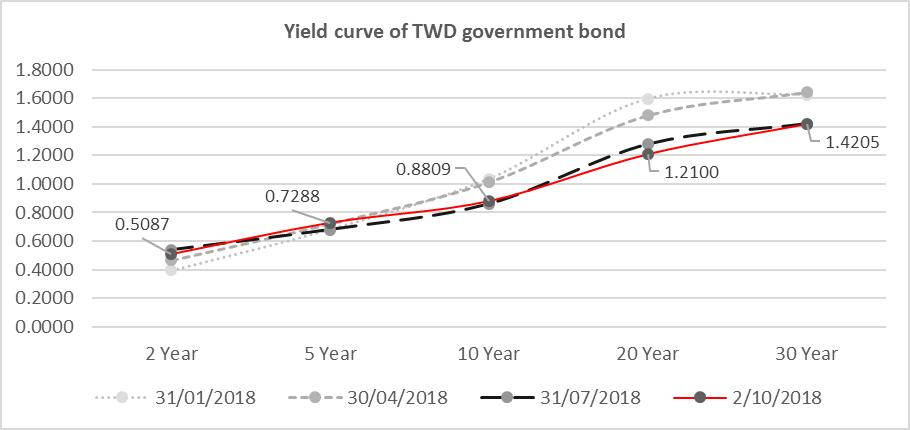

The banality of the Taiwan dollar denominated bond market can also be inferred from its yield attractiveness, or unattractiveness to be specific. The flattening yield curve of Taiwan dollar denominated government bonds might imply investors are cautious about the macroeconomic outlook in the future given the ongoing and seemingly unending trade war, and expected Fed rate hikes.

However, the most "eye catching" feature is the low-yield rate. Currently, the US treasury yield rates of 2-year tenor and 5-year tenor are around 2.82 and 2.94 respectively, which is considerably more attractive than the Taiwan's 0.51 and 0.73 ( fig. 3 ).

Fig. 3

Source: Taipei Exchange

Without a significant proportion of global investors holdings due to its unattractive yield rate, the Fed rate hikes and a strong US dollar environment consistently fails to trigger a sell-off in Taiwan dollar denominated fixed income. This explains the banality of the Taiwan dollar denominated bond market. It is under this background that the ABR is announcing the top sellside firms in the Taiwan dollar denominated bond market.

To view the rankings of the top banks in the secondary market and top bank arrangers for 2018 please click here.

Top Banks in Asian Currency Bonds 2018 methodology

The Asian Local Currency Bond Benchmark Review 2018 surveyed over 380 institutional fixed income investors who are active in 10 Asian currency bond markets: China ( onshore and offshore i.e. CNH ), Hong Kong, Indonesia, India, Malaysia, Philippines, Singapore, Taiwan and Thailand.

Survey participants included asset managers, banks, and insurance companies from both domestic and international institutions. They were asked to rate the best banks or securities companies across a series of buying criteria and identify their trading counterparties in the secondary market. The banks are ranked in each market according to their wallet share; the names of the top three are published. Additionally, investors nominated the best banks/securities houses as arrangers in the corporate and government primary markets in terms of the quantity and quality of the issues.