now loading...

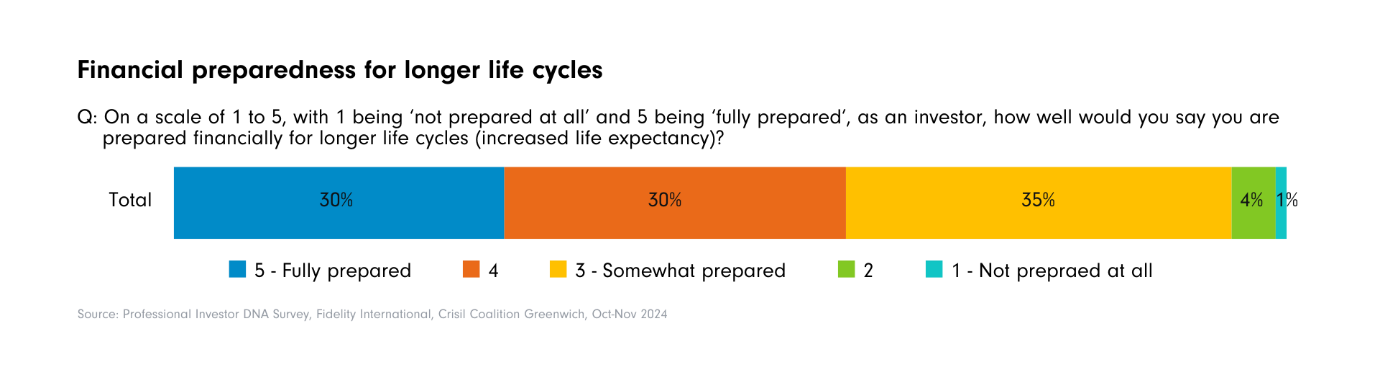

Only 60% of professional investors say they are fully or almost fully financially prepared to support clients in living longer in retirement, with a high proportion of respondents ( 40% ) highlighting a lack of preparedness, a new survey finds.

Fidelity International's Professional Investor DNA Survey, developed with Crisil Coalition Greenwich, covered over 120 institutional investors and intermediary distributors across Europe and Asia.

It comes at a time when the global population is experiencing a significant demographic shift towards an older age structure. According to the World Health Organization, the number of persons aged 80 years or older is expected to triple between 2020 and 2050 to reach 426 million.

“The global retirement challenge and the pension funding gap are not new, yet these issues continue to accelerate significantly, as populations are expected to live longer, and to some extent, be healthier and more active in retirement,” says Katie Roberts, global head of client solutions at Fidelity International.

“While the retirement challenge requires local solutions, what is clear is that state support overall is likely to be less going forward, with individuals becoming increasingly responsible for financing their retirement.

"To generate enough capital to support this extended life span, professional investors have a key role to play in providing their clients with relevant long-term solutions, whether it be through workplace investing or customized, private solutions to prepare for retirement and ensure their clients continue to be invested in retirement,” she adds.

Products and solutions

An important element for retirement preparedness includes identifying the appropriate financial investments and solutions to support clients in creating sufficient wealth in retirement, according to the report.

When asked if there are currently enough products and solutions in the market addressing the needs of an increasing life expectancy, only 57% of professional investors agreed. While the majority of respondents are comfortable with the number of solutions available, it also highlights the need to further develop the product and solution range geared towards longevity challenges.

"These results show that the majority of professional investors believe there are enough products and solutions available in the market, yet 43% disagree. This highlights an opportunity to further develop innovative financial solutions to alleviate any provision gaps,” says Roberts.

Portfolio allocation

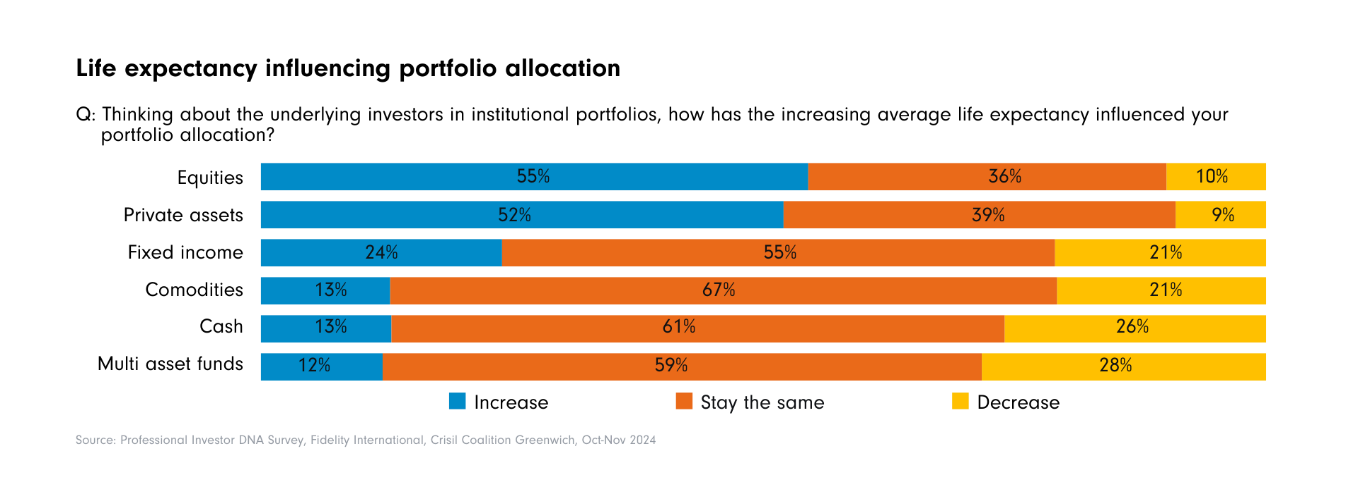

In terms of asset allocation, the study shows that investors are leaning towards equities and private assets as a means of increasing the risk-return profile of their portfolios in anticipation of longer life expectancy for their clients.

Over half of investors ( 55% ) confirmed they expected to increase their exposure to equity, closely followed by private assets ( 52% ) and fixed income ( 24% ).

Meanwhile, the survey points to potential decrease in exposure to multi-asset funds ( 28% ), cash ( 26% ) or fixed income ( 21% ).

“Interestingly, the findings suggest that when planning for retirement, investors are focused on increasing their allocation to more risk-on asset classes to accumulate wealth over time,” Roberts notes. “What this may not show is how the portfolio allocation changes when clients transition from a wealth accumulation phase to a decumulation phase in retirement. Indeed, in retirement, one might consider products that provide more accessible and flexible liquidity.”

“Preparing for retirement remains complex, especially when considering the changing market environment, local specificities including regulation, pensions policy and frameworks, or age of retirement. In parallel, investors must consider the difference between investing for retirement and investing in retirement which involves ensuring sufficient funding throughout the entire extended life cycle,” she adds.