now loading...

Equities may do well next year, with earnings growth expected to accelerate slightly in both developed and emerging markets, but investors need to be cautious, depending on how the global economy performs.

“We've seen three years of flattish earnings, and next year, we do expect developed markets earnings growth of 8%, and emerging markets 11%,” says Marcus Poppe, co-head, European equities, DWS, at the asset management firm’s Market Outlook 2024. “Nevertheless, as a word of caution, we are slightly below consensus expectations, around 3%.”

The challenge for investors is whether major central banks, particularly the US Federal Reserve and the European Central Bank, will be forced to cut interest rates in order to prevent a drastic economic slowdown in their efforts to control inflation.

“Can central banks lower rates or are they forced to lower rates? That will have very significant impact on where you should position in equities because if they are forced to lower rates, this means the economy is actually getting worse, then earnings will disappoint and that's not a good sign for equities,” Poppe says.

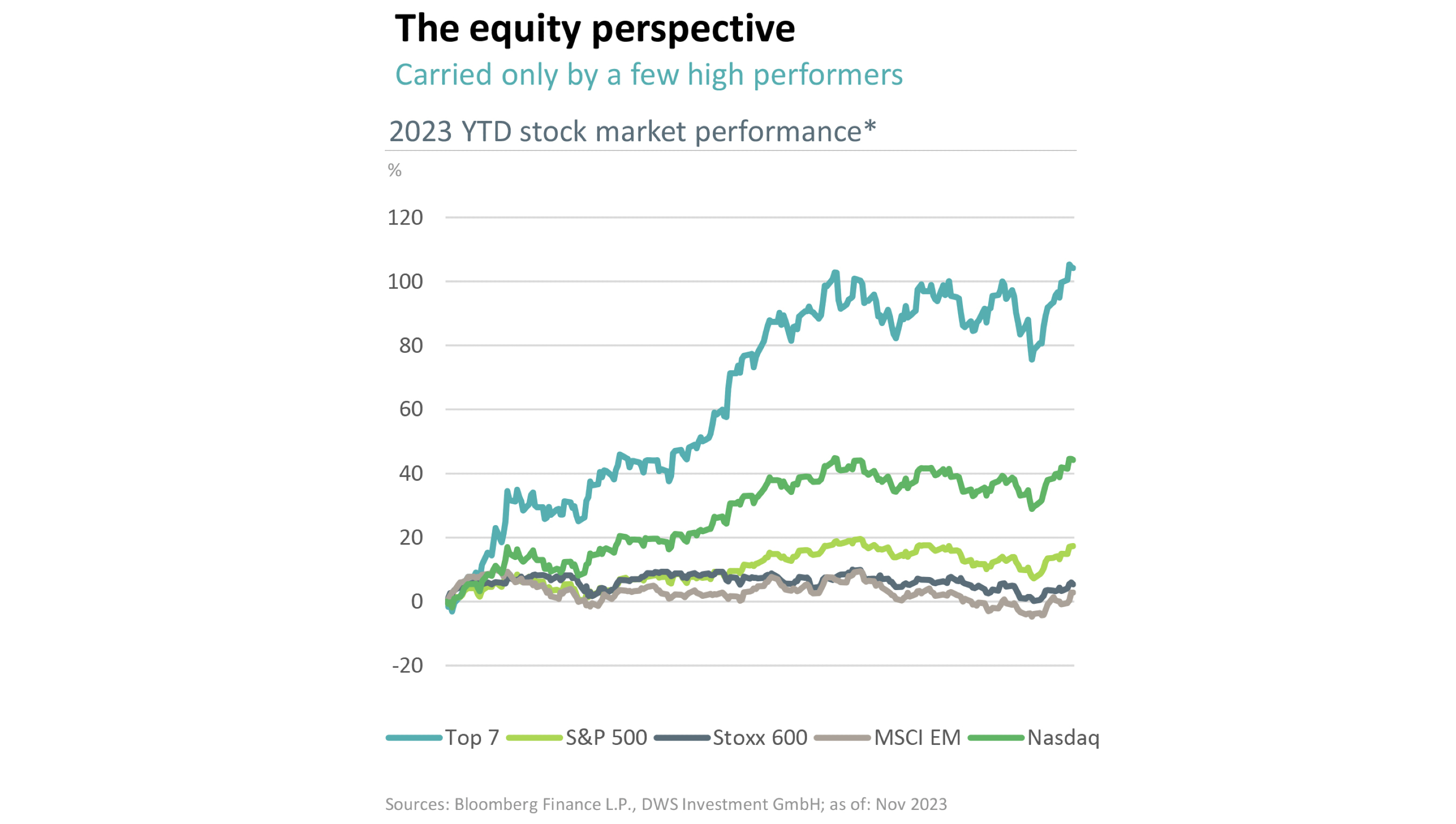

At present, the big-cap equity market based on the S&P500 is highly concentrated with the seven biggest stocks making up about 29% of the total market capitalization. These include Apple ( AAPL ), Alphabet ( GOOGL, GOOG ), Microsoft ( MSFT ), Amazon ( AMZN ), Meta ( META ), Tesla ( TSLA ), and Nvidia ( NVDA ).

Often referred to as the “The Magnificent Seven”, these stocks have dominated the S&P500 since the start of the year because they have been the best performing stocks based on their fundamentals, earnings growth, and investment themes. Investors have flocked to these stocks in a big way, resulting in a lopsided positioning of the index.

Data from Goldman Sachs indicate that the “magnificent seven” stocks have gained 71% while the other 493 stocks have added just 6%. The S&P500 has gained 19% as of November 16, based solely on the contribution of the larger stocks to the index.

“That's why we say the “magnificent seven” stocks have a “licence to kill” ( in reference to the 1989 James Bond movie of the same title ). As an active fund manager or investor, if you're not in those stocks, it's really getting hard, and therefore those seven companies, they really do suck the capital into them. And it almost becomes a self-fulfilling prophecy,” Poppe says.

Investors cannot be blamed for investing heavily in these stocks because of their strong outperformance particularly since May 2023. These companies are also engaged in the latest and most popular technology investment themes, which are resonating with investors and supported by strong fundamentals.

The earnings expectations for these companies are constantly being revised and hence, investors and fund managers have to follow their earnings performance.

On the flip side, valuations of the “magnificent seven” stocks are skyrocketing, trading at an average forward price-to-earnings ratio of 33.5, compared with the S&P 500's P/E of 18.3.

“Investor positioning is clearly one sided. Everybody is on this ‘magnificent seven’ train. Everybody is hiding in those stocks because overall, in equities you see a lot of risk aversion elsewhere. So, positioning could be an issue coming into next year. But for the time being, we remain of the view that the fundamental strength of those business models supports them. But just be aware, if things are better than we do expect, if the economy accelerates more, and inflation comes down more, the real Goldilocks scenario, then most likely investors will also seek investments outside of those names because then they can also get earnings growth at a much cheaper valuation. So that has to be kept in mind,” Poppe says.